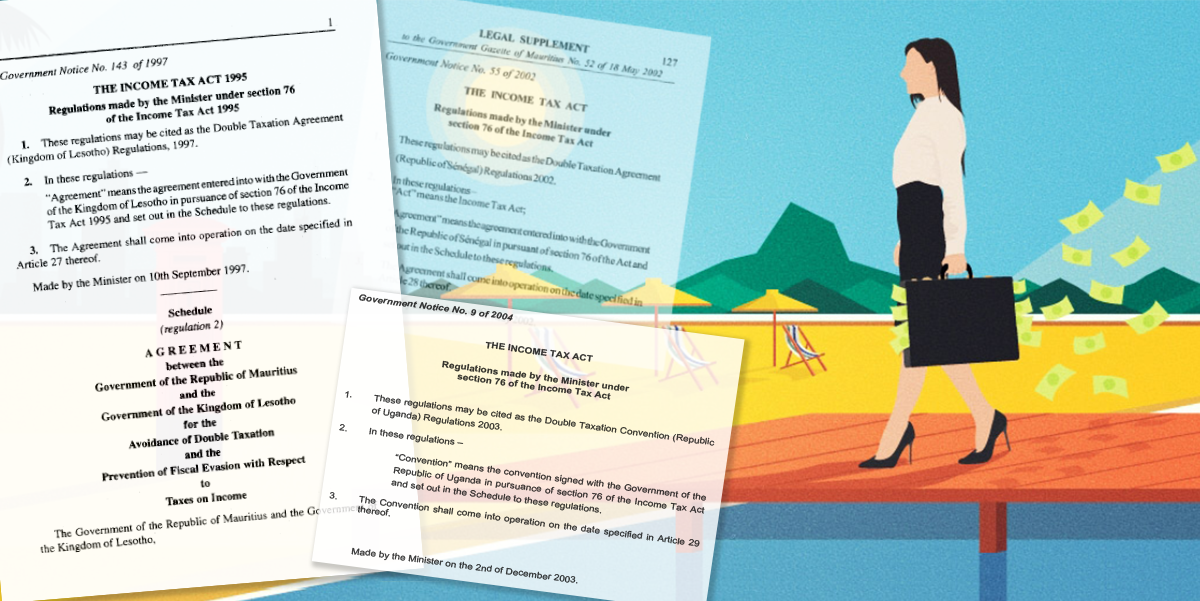

Soon after we started searching hundreds of thousands of files sent anonymously from the island nation of Mauritius, we asked ourselves: What are all these “double taxation agreements” or “tax treaties” we keep seeing?

Time and time again, we read emails and documents from lawyers and multinational corporations asking to use treaties between Mauritius and countries in Africa, Asia and the Middle East to reduce taxes paid to the other countries.

But what are they? How do they work? And why are they so controversial?

ICIJ spoke to Martin Hearson, lead researcher on international tax at the International Centre for Tax and Development based in Brighton, England, at the Institute of Development Studies.

What is a tax treaty?

There are about 3,000 of these bilateral agreements around the world. The main function is to carve up the right to tax businesses and people who earn money across borders and divide up that tax between two states.

What is the purpose of a tax treaty?

Tax treaties really came into being about 100 years ago as business started to become more international. Businesses started to find they were receiving tax claims by multiple states for the same money. The idea was that they should only pay taxes once. States signed these agreements to make clear in what situations one state would get taxes and in what situation the other state would get taxes.

That original reason is no longer quite as important as it was in the first half of the 20th century. Today, most large capital-exporting states already take steps unilaterally to prevent people and businesses who make money abroad from paying tax twice. They offer a credit for any taxes paid abroad or they just exempt foreign income.

However, that original reason for wanting to avoid double taxation is not entirely gone, because there are always going to be some differences in the way that countries treat profits.

Apart from avoiding double taxation, why do countries sign them?

The other main function of tax treaties, especially from the perspective of developing countries, is about tax competition. Tax treaties are effectively an incentive offered only to investors from a particular country. Many treaties signed by developing countries were done in the hope of attracting investment.

This helps understand why they are signed, but also perhaps why developing countries have been reluctant to rock the boat when their tax treaties are abused. I think there’s a balancing act in the mind of politicians who want to attract investment but also want to be able to tax that money.

Tax treaty? Double taxation avoidance agreement? DTT? Double taxation treaty? DTAA? What’s with all the confusing terms and abbreviations?

I don’t call them double taxation treaties. I call them tax treaties. Because helping companies avoid paying double tax is not really the main thing that they do. The main thing they do is to take a set of standards for taxing companies, that was developed among the wealthy OECD states, and turn it into hard, enforceable law. This often doesn’t seem to work very well for African countries.

How did tax treaties go from being about avoiding double taxation to facilitating double non-taxation?

It’s the use of the tools – designed for one function – to do something different to get around paying taxes at all or at least to reduce taxes.

When states sign a tax treaty, they voluntarily accept restrictions on their ability to tax cross-border transactions. Those restrictions are legally binding.

As tax havens emerged, and certain states realized they could use international tax efficiencies to attract business, businesses and tax advisers also realized they could minimize the tax they had to pay around the world.

So, the same restrictions that states had accepted on their ability to tax cross-border payments were now the main instruments being used to prevent those states from taxing them at all. Or to prevent states from taxing them in ways the state didn’t intend when it signed that treaty.

The terms of tax treaties are public. If nothing is secret about them, what’s the problem?

There’s a difference between tax avoidance and tax evasion. People often tend to think about tax havens in terms of this secret space where money gets hidden.

In order to evade taxes, which means you want to break the law by not declaring income that you should, you need to hide it.

Tax avoidance, on the other hand, exploits the way the law is written. For example, a tax treaty can be used to gain an advantage which wasn’t the original intent of the treaty. The tax authority isn’t able to do anything about that in the immediate term because the taxpayer is legally entitled. In the longer term, what you need to do is change the law. You need to change the tax treaty, which is hard to do because you need both sides to agree to it.

In the case of Mauritius, it’s been difficult for countries to persuade Mauritius to include in the treaty the kind of wording you need to prevent it being used to avoid taxes. Mauritius has been reluctant to do that, which would allow African countries to tackle tax avoidance.

What does the research tell us about whether double taxation agreements increase investment?

The bottom line for an African policymaker is that there is no reliable evidence to support the idea that signing a particular tax treaty will bring investment into a country.

There are some studies that suggest some kind of effect, there are others that suggest no effect and even some studies that suggest a negative effect. We don’t have convincing consensus that tax treaties bring investment to poorer, developing countries.

Between developed countries, it’s a bit different. In that case, because investment flows are much more complex, the scope for double taxation is higher. So I think there is evidence to support the idea that treaties work. But for an African country, the evidence is not there.

You have to look at each treaty in terms of the tax systems of the two signatories and the economic activity between them to understand whether it’s really necessary.

Who or what was behind promoting tax treaties, and why?

The emergence of the tax treaty regime begins with a combination of two drivers, which are still very active today.

First, multinational companies, which still say: ‘We’d like to invest here, but we’d like a tax treaty to lower our taxes.’ Lobbying by businesses is still a very strong driver of the expansion of the tax treaties.

Second, a combination of lawyers, tax professionals, negotiators and civil servants. This community of people – from the very beginning – have drafted and negotiated treaties and formulated the concepts and the narrative about why they matter. This community is still very active today in terms of championing the idea that tax treaties are a good thing.

What about the Organization for Economic Co-operation and Development, IMF, African Union?

In the last 50 years, during which the African continent has become increasingly covered by tax treaties, there are periods of time in which there has been an active effort by international organizations to promote tax treaties.

In the 1990s, the OECD was active in trying to reach tax administrations in Africa and encourage them to negotiate tax treaties. UNCTAD, the U.N.’s trade and investment body, also promoted tax treaties as a means of promoting investment.

In the present day, the World Bank and IMF are much more skeptical because they’ve seen the evidence. The OECD is now promoting a package of international agreements and initiatives of which tax treaties are just one part.

Why does so much tax treaty research focus on developing countries?

One of the reasons we focus on developing countries is that it’s less clear what they’re getting from tax treaties.

Another reason is that the kind of tax-avoidance schemes that developing countries face tend to be less complex and to rely on fairly simple tax treaty clauses. This makes tax treaties one of the main instruments used to avoid tax in developing countries.

The final point is that developing countries are at a big disadvantage in terms of their capacity to tackle this, because their domestic law and their administrative capacity may not be as well-developed as those of developed countries, leaving them open to treaty-shopping structures which wouldn’t necessarily work in a developed country.

Why should anyone care?

Tax treaties do this really strange thing. They take something that we consider to be a fundamental part of our democracy – tax policy and tax rates, which elections are won and lost over – and they take it out of the hands of politicians. They lock it down in a binding treaty, which often has been negotiated by bureaucrats and rubber-stamped by politicians, rarely with any parliamentary scrutiny.

If you care about democratic control of how big corporations are taxed, then understanding how much of that happens without politicians being able to control it is one reason you should care.

How would you describe Mauritius’ role in the international landscape of tax treaties?

Mauritius is the lynchpin of many tax avoidance structures in Africa. There are other jurisdictions involved, like the Netherlands, but Mauritius is really the top of the list. And the position that Mauritius occupies is really down to its tax treaties.

Mauritius is one of a number of small island states that has realized that financial services is one sector in which it can compete. It’s decided that the way it’s going to establish that is through a network of tax treaties. The strategy of enabling tax avoidance as a way to achieve that is the choice Mauritius made.

It’s amazing when you look at it how many African countries have treaties with Mauritius, given that those treaties open those countries up to the risk of tax avoidance. Mauritius is an African country, and I think it has used that status to give it a sense of legitimacy.

I think Mauritius is the African tax haven. It’s the country that you use if you want to avoid taxes in a large number of African countries if you’re a multinational investor. It’s the tax treaty network that gives it that.

What can or should Mauritius do?

It’s a really pivotal moment. Governments, through the OECD, have agreed on a way to change tax treaties that will make it harder for companies to avoid tax and easier for tax authorities to stop it.

Mauritius hasn’t been particularly forthcoming in its willingness to see its treaties with African countries amended. It’s managed to avoid being blacklisted by the OECD and the EU. It’s done that through some clever changes to the way its tax system works so that they comply with the letter of the rules but not necessarily the spirit. It looks like Mauritius is doing its best to continue to play this role of being a conduit for tax avoidance in Africa.

I think what Mauritius should be doing is two things. One is cleaning up its act. That is, accepting that while there are reasons to have financial centers, the tax-avoidance dimension needs to go. Then also looking at diversifying its economy; Mauritius is still a developing country, and it needs to look at alternative strategies for development.